Merchant cash advances have the convenience of being easy to get. They can also be set up quickly, which makes them popular among some business owners. However, their convenience comes at a cost.

Business cash advances are very expensive. And, in some cases, businesses that use this type of financing end up worse off.

In this article, we discuss the best way to refinance an MCA. We also discuss some of the potential pitfalls of using the wrong financing options to refinance a cash advance. Here is a list of what we cover:

- The financial dangers of cash advances

- Why using an MCA to refinance a cash advance is a bad move

- Why you should not use MCA reverse consolidations

- The right way to refinance a business cash advance

- The importance of working with a CPA

If you are not familiar with cash advances, you can learn more by reading this article and this one.

Why are cash advances financially dangerous?

If you are reading this article, you probably have a business cash advance. You also have a good idea of how those weekly (or daily) payments quickly add up and become a problem. But MCAs can be dangerous for many reasons. Here are the most important:

1. Borrowers tend to focus on the payments only

Companies that get cash advances often focus on the weekly payments, instead of focusing on the total affordability and cost of the loan. They believe that if they can afford to make the weekly payments, everything will be fine. Unfortunately, things don’t always go as planned.

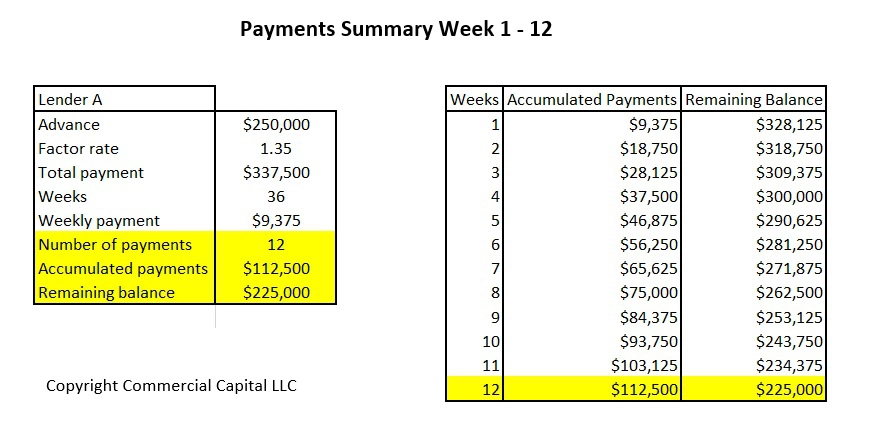

Let me explain with an example. A medium-sized company needs a cash advance that has these features:

- Advance amount: $250,000

- Factor rate: 1.35

- Period: 36 weeks

This cash advance has a weekly payment of $9,375. This amount is calculated by multiplying $250,000 by the 1.35 factor rate (which equals $337,500) and dividing the result by the 36 week period.

If the company has sufficient revenues at the time, and needs the money urgently, they may think they can afford the $9,375 weekly payment. This view is often short-sighted, though.

Business owners don’t consider the long-term consequences of these high payments. Will they be able to cover this payment every week – for the whole 36 weeks? They may think so, but most business owners are overly-optimistic about their future. Consider, what happens if:

- Their revenues go down?

- A project does not materialize?

- They lose an important client?

- Their cash flow slows down?

Actually, so-called unexpected problems are surprisingly common. Something happens to revenues. Or, there is an unexpected expense. Consequently, they are unable to keep paying the cash advance. Ultimately, they end up in more financial trouble.

2. Cash advances are used incorrectly

Cash advances are often used incorrectly. They are applied to situations that are not best solved with an advance. This makes problems worse.

For example, cash flow problems usually can’t be fixed with a cash advance. Neither can profitability problems, collections problems, or bad financial management. However, business owners often try to use a cash advance in these situations. As a consequence, the company ends up in a worse financial position.

3. Companies “stack” more than one cash advance

When faced with growing financial problems, some companies opt for an additional cash advance. They hope that the additional cash advance will fix the problem that the first advance couldn’t fix.

Having multiple cash advances is an expensive mistake. It is referred to in the finance industry as “stacking.” Stacking merchant cash advances often leads to business failure.

Even getting a new and supposedly “cheaper” advance to refinance an older advance is often an expensive mistake. We go over this in the next section.

Don’t refinance a cash advance with a new one

Refinancing a business cash advance with another one is a common financial mistake. Even if the transaction is refinanced with an MCA that has a much “lower” weekly payment.

To understand why, you must first understand an important detail about merchant cash advances. Unlike conventional business loans, cash advances are not amortized. Amortization allows loans to keep track of “interest” and “principal” costs separately. Paying off the principal early often brings savings to the borrower. It closes the loan, so the borrower saves money by not paying any additional interest.

Cash advances, on the other hand, lump both principal and fees into a single total payment cost. For example, a $250,000 cash advance with a 1.35 factor rate has a total payment of $337,500. The borrower has to pay a total of $337,500 to the lender to close the loan, even if they pay off the loan early. There is no separation of “principal” and “interest,” as in an amortized loan.

The following image shows an example with the MCA we just described. After 12 weeks, you can see the accumulated payments and remaining balance. The remaining balance is the amount that must be paid to close (or refinance) the cash advance. It’s just the Total Payment less the Accumulated Payments. Paying it off early does not result in a cheaper payment since there is no “unearned interest” like in conventional loans. The bottom line: there is no financial advantage to the borrower to pay off early.

Their high interest rates coupled with their lack of amortizations make cash advances an expensive financing option. Using a new cash advance to refinance an existing one is extremely expensive. You are using an expensive and non-amortized product to refinance another expensive and non-amortized loan. Actually, a large part of the new MCA goes to pay off the interest cost on the first cash advance. Ultimately, you end up paying expensive “interest on interest.”

Could an MCA reverse consolidation help you?

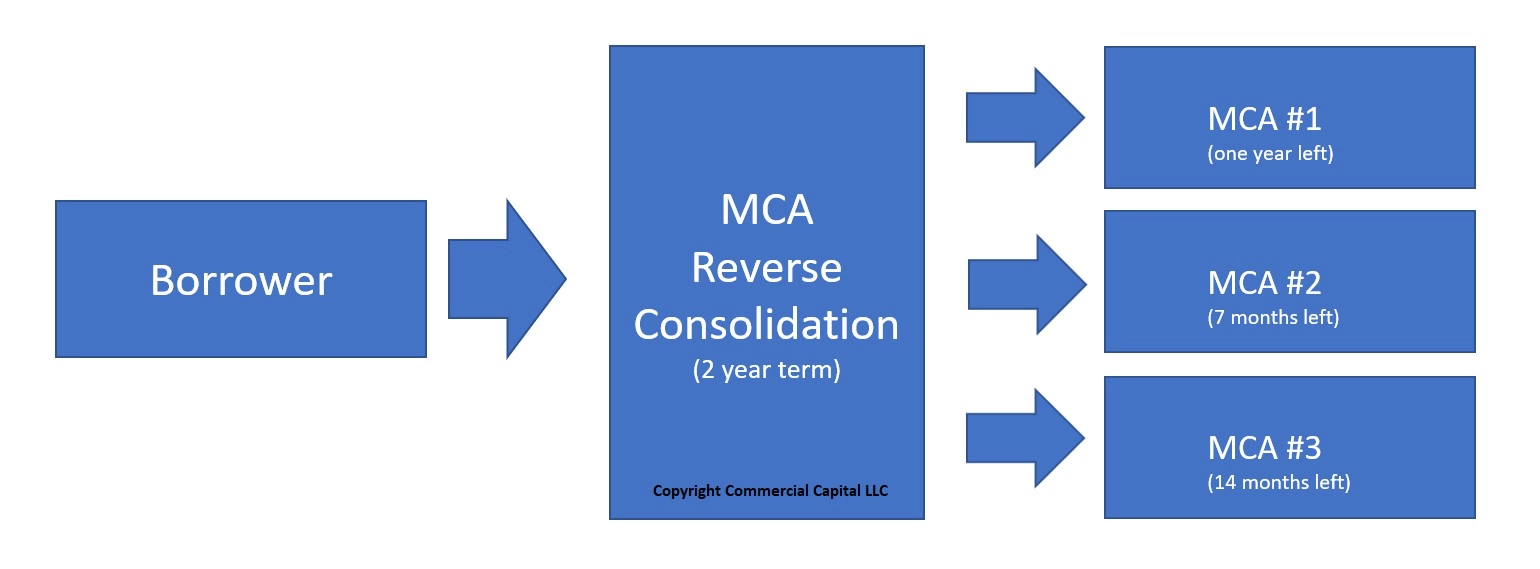

An MCA reverse consolidation is a product that allows you to pay off multiple cash advances by taking a new one. However, this type of cash advance refinancing adds a twist.

The reverse consolidation lender issues a new cash advance to you, while taking over the weekly payments for your other advances. Basically, you make a single payment to the lender, who then takes care of your other cash advances.

This last point is an important detail. The reverse consolidation company does not immediately pay off your open MCAs. Instead, they just take over the weekly payments until the open MCAs are paid off. This image shows how they work.

Reverse consolidations may appear attractive at first. Your payment to the new lender is usually lower than the total weekly payments to the other lenders. That looks like an advantage, doesn’t it?

As you probably imagine, the new loan is for a much longer term. This provides a lower recurring payment, but for a longer time. Ultimately, your company ends up with a much higher total loan payment.

The problems with MCA reverse consolidations

Why does the reverse consolidation lender take over your other payments, instead of just paying off all the open MCAs? It would be to your advantage. You are better off with just a single open loan, instead of multiple loans. Furthermore, it wouldn’t cost the reverse consolidation lender anything extra. The cost of paying off the MCA is the same regardless.

Reverse consolidation lenders make only weekly payments instead of paying them off for two simple reasons. It increases the lender’s rate of return while reducing their risk (exposure) significantly. This last point is very important. Let me take you through a hypothetical example.

Let’s say a business has 3 existing MCAs and takes on a reverse MCA consolidation loan. They hope the lower payment will help make their cash flow manageable.

Unfortunately, the business loses a customer and misses a few payments to the reverse consolidation lender. Initially, the business is hit with a few penalty fees from the lender. Let’s say that the situation continues and the business eventually defaults on the reverse consolidation MCA.

Ask yourself, will the reverse consolidation lender continue to pay the other open MCAs? Let’s ask the question differently. What is the lender’s incentive to keep making the weekly payments to your other lenders – if you are no longer paying? Stopping the payments limits their exposure and risk.

Continuing with this example, what do you think will happen if the reverse consolidation lender stops making weekly payments to your other MCA lenders? My guess is that these lenders will charge you some penalties. But ultimately, if they don’t get paid, they will declare your cash advances in default.

At this point, the company has four stacked merchant cash advances: the three conventional MCAs and a reverse consolidation MCA. Hypothetically, you could end up with four defaulted advances. Realistically, no business could survive that.

What is the solution? Stick to the basics

If you need to refinance an MCA, the solution is pretty simple. You must refinance it with affordable conventional financing. This is the only way you will be able to get out of an MCA without paying a fortune. Note, the transaction will still be expensive. But that is because the MCA you are refinancing is expensive.

The best options to refinance an MCA are as follows:

Small Business Administration-backed loans

SBA-backed loans are one of the best tools to refinance or consolidate business debt. The SBA allows lenders to provide market-priced loans to companies that couldn’t get one otherwise. This includes companies that have less-then-perfect situations.

Getting an SBA-backed loan requires some paperwork and diligence. Finding the right lender may take some time. However, the effort is well worth the savings.

Asset-based lending

Asset-based financing may help your company if it has assets like machinery or real estate. An asset-based loan enables you to borrow against specific assets. In the case of machinery or real estate, the lender can use an amortized loan at reasonable prices.

Asset-based loans are somewhat more expensive than SBA-backed loans. However, they are easier to get and have fewer covenants.

Accounts receivable financing

One last option to consider is accounts receivable factoring. This solution can help you if your company’s total accounts receivable exceeds your total debt. While this situation is unusual in companies that have excess MCA debt, we have seen it in the past.

Basically, you finance your open invoices and use the proceeds to close the cash advances. Getting factoring is much easier than getting an asset-based loan or an SBA-backed loan. However, factoring costs more than these alternatives.

Talk to your CPA

Refinancing your company’s debt is an important decision. Especially if your MCA debt load is very high. The wrong financial choice could be disastrous. Therefore, we have one important recommendation.

Hire a CPA to work with you. They can help you understand your alternatives and suggest specific solutions to your situation. While CPAs are not cheap, hiring one is much cheaper than the alternative. Especially when the alternative spells financial disaster